Are you buying a property? Congratulations! It’s indeed a giant milestone. At the same time, it’s the biggest financial commitment you’ll ever make. With more than 100 lenders, a number of mortgage types, and rapidly evolving interest rates, it could be difficult to navigate home loans Australia!

Yet, the wisest borrowers are not lucky, they are rather well-informed. They know how to smartly compare home loans the right way.

Imagine this: You’ve found the home of your dreams anywhere in Sydney or Melbourne. The agent handed you a bunch of glossy brochures, each filled with rates, offers, and some unclear loan jargon. How might you select the best deal and prevent any long-term confusion or regret?

This guide is your trusted roadmap to smarter home loan decisions in 2025.

A Quick Summary

In this 2025 guide to compare home loans, you can discover the offerings of top home loans Australia, unlock key mortgage types, monitor changing interest rates, and sidestep costly errors – fast! Filled with expert suggestions, real-world examples, and a clear chart, this will inch you closer to smarter decisions.

Why It Pays to Compare Home Loans: The 2025 Advantage

Picking the right home loan in 2025 transcends chasing the lowest interest rates. The landscape of lending in Australia has transformed with the emergence of more digital leaders, edgier features, and faster approvals.

However, the real edge is this – the true comparison can save you more than $80,000 across the lifetime of a typical 30-year loan.

- Some of the Core Takeaways:

- Striking a comparison between different home loans Australia isn’t only about rates, but is also about looking at flexibility, fees, and features.

- Slight differences in interest rates (even 0.25%) = thousands saved!

- Lenders can now provide fully customized solutions for those taking up home buying loans, investors, and self-employed individuals (check low documentation home loans).

- Early repayments and offset accounts could shave years off your mortgage.

Expert Take: “In 2025, there has never been any major gap between the ‘best’ and ‘average’ loan offers. Savvy borrowers utilize each tool to negotiate, compare, and personalize their deals.” – Kelly Tran, Senior Mortgage Broker, Sydney

Let’s now dive deeper into what truly matters when you start comparing?

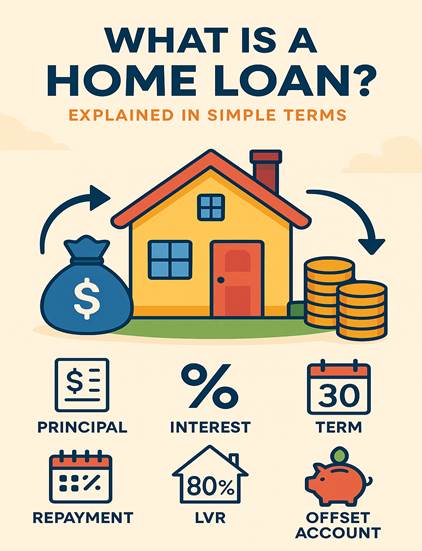

What is a Home Loan? Explained in Simple Terms

A home loan or mortgage refers to the money borrowed from a lender to make a purchase of a property. You need to repay the amount – plus the interest rates – in frequent instalments over 20–30 years.

Most of the loans in Australia are “secured” (the loan is backed by the property). However, not all mortgage types are equal. From sophisticated offset accounts to the basic variable loans, your choice could quite radically shape your financial future.

- A Quick Breakdown of the Home Loan Jargons

- Principal: The actual loan amount borrowed.

- Interest: The overall cost paid to the bank/lender for using their money.

- Term: Total length of the loan (typically 25–30 years in Australia).

- Repayment: Regular (generally fortnightly or monthly) payments.

- LVR (Loan-to-Value Ratio): The size of the loan compared to property value.

(E.g., $500k loan on around $600k property = approximately 83% LVR) - Fixed vs Variable: Whether the interest rate remains the same or evolves.

- Offset Account: A transaction account linked to your home loan, which minimizes the overall interest you pay.

Now, have a look at the basics. Let’s now glance at the numbers.

Comparing Interest Rates: A Game Changer When You Compare Home Loans

- Why Does Interest Rates Matter the Most

The interest rate is a key factor in your total loan cost. Even a slight difference—like 6.20% vs 6.50% - could cost (or save) you thousand bucks!

Let’s now see how this process actually works:

| Loan Amount | Interest Rate | Monthly Repayment | Total Interest Over 30 Years |

| $600,000 | 6.20% | $3,679 | $724,440 |

| $600,000 | 6.50% | $3,795 | $766,200 |

| Difference | 0.30% | +$116/mo | +$41,760 |

Don’t Forget This Comparison Rate

Australian law needs lenders to showcase a transparent comparison rate, a single percentage that perfectly blends the interest rate and standard fees. It helps you compare home loans fairly and accurately.

Pro Tip—Never ever forget to check the comparison rates thoroughly to get a clear, honest picture in your head!

Quick Stat: More than80% of Australian borrowers could actually save an average of $3,000 per year just by comparing their existing loans to new offers (Finder, 2024).

The Main Mortgage Types in Australia

Understanding your mortgage types is the number-one step in picking the right product, especially when you compare home loans. Below is a quick breakdown; each complements a different borrower profile:

1. Variable Rate Home Loans

- Interest rates can move up or down with the shifting market/cash rate.

- Usually provide more flexible features (such as extra repayments, redraw, etc.).

- Ideal for: Borrowers who demand flexibility and can mitigate some risks.

2. Fixed Rate Home Loans

- Lock in your interest rate (maybe for one, two or five years).

- Gives payment certainty – perfect option for budgeting.

- Drawback: Limited flexibility (additional repayments often capped).

3. Split Loans

- Divide your loans: part fixed and part variable.

- Combines security with optimum flexibility.

- Perfect for: Those who need a safety net but don’t want to miss out in case rates drop.

4. Offset Account Loans

- Get a transaction account linked to your mortgage.

- Each dollar in the account “offsets” the balance of your loan, minimizing interest.

- Incredibly huge savings for diligent savers.

5. Low Doc Home Loans

This one is an ideal option for freelancers or self-employed people who might not have traditional payslips. Fewer income docs are required, but they typically come with slightly higher interest rates and more stringent lending rules.

6. Loan for First-Time Home Buyers

Special products for Australians buying their first home, with government help, lower deposits, and special incentives.

How to Compare Home Loans Confidently: Step-by-Step Checklist

Is it truly challenging or stressful to compare home loans in Australia? Follow this quick, actionable checklist to break down the decision process. This process applies regardless of whether you are a new buyer, a home loan applicant, an investor, or simply refinancing with the same lender!

1. Begin with Your Borrower Profile

- Are you a first home buyer, investor, upgrader, or self-employed?

- What’s the size of your deposit? (around 20%+ helps in avoiding LMI; below 10% might limit choices)

- Income stability: Contractor, business owner, Full-timer or part-timer?

- How long do you need to plan to stay on the property?

2. Get Essential Loan Information

The moment you compare home loans, consider collecting these details from every lender or online aggregator:

- Interest rates (both comparison and advertised rates)

- All fees (application, annual, monthly, redraw, discharge, etc.)

- Mortgage types offered (fixed, variable, split, offset, interest-only)

- Loan features (offset account, redraw, extra repayments or repayment frequency)

- Minimum deposit as well as LVR requirements

- Special features: Construction loan, green home loan, etc.

Always use an online comparison tool like Canstar, Mozo, RateCity, Finder, etc. or a spreadsheet for recording and comparing details, side by side.

3. Shortlist the Top Contenders

- Rank by comparison rate, not only the interest rate.

- Note the overall cost over the full loan term. Refrain from just chasing the lowest repayments.

- Thoroughly assess features depending on your needs (offset for savers or redraw for flexibility).

- Always check if you are eligible for incentives for new home buyers or government schemes.

4. Read the Fine Print

- Are there penalties or any break costs for early repayments?

- What’s the flexibility to switch between fixed and variable rates?

- Is there any honeymoon/introductory rate that might soar later?

- Are there any lender restrictions based on property type, postcode, or employment?

5. Always Ask the Right Questions

Engage your lender or broker with these questions –

- Can you beat or match a competitor’s rate?

- What’s the average approval time for your loans?

- How often do you review or pass on rate cuts?

- Are there any hidden fees or conditions, which could apply in my situation?

So, are you all set to shortlist? Let’s now delve into some of the most effective and popular comparison tools, and give you an insight into how you can use them confidently.

Comparison Table: Popular Home Loans Australia

| Loan Product | Typical Interest Rate | Comparison Rate | Main Features | Best For |

| Basic Variable | 6.25% | 6.35% | Low fees, extra repayments | Budget-focused buyers |

| Fixed Rate (2 years) | 6.45% | 6.45% | Rate certainty, limited redraw | Planners, risk-averse |

| Offset Account Loan | 6.30% | 6.50% | Offset, redraw, flexible pay | High-income/savers |

| Split Loan | 6.20%–6.50% | 6.40% | Mix of fixed & variable | Balanced risk-takers |

| Low Doc Home Loans | 7.10%+ | 7.30% | Self-employed, higher rates | Freelancers/businesses |

| First Home Buyer Loan | 6.10%+ (with gov. support) | 6.18% | Lower deposit, incentives | First property buyers |

Keep in mind, rates are indicative. So, always check the latest MoneySmart, market aggregators, and lender websites.

- How do I know which lender provides the best deal?

Put these steps into practice:

- Compare at least 5+ lenders that include a combination of regional banks, major banks, and online/digital lenders.

- Use the comparison rate as it combines the most fees and advertised rate for a truer picture.

- Carefully read reviews on platforms like ProductReview.com.au, Finder, Trustpilot, etc. to get honest insights into service quality.

- Take customer service, digital tools, and accessibility into account.

All set to apply? Here’s everything you will require.

- What documents do you need for a home loan Australia application?

- Proof of ID (passport and driver’s licence)

- Income verification (payslips, tax returns, and bank statements)

- Savings/deposit evidence

- Contract of sale (in case you’ve found a property)

- Extra docs for low-document home loans, such as BAS statements, accountant’s letters, business financials, etc.

- Can I refinance my current home loan to save money?

Yes, absolutely. Refinancing is one of the most effective ways to access better interest rates, minimize repayments, or discover new features.

Watch out – some loans have break costs, particularly if fixed. Hence, weigh the savings against any exit fees.

New Buyer Home Loan: An Important Guide

Are you looking to enter the market for the very first time? If yes, then you should look out for the followings –

- Government grants (First Home Owner Grant, stamp duty concessions, and shared equity schemes)

- Lenders providing lower deposit requirements (as little as 5%)

- Special discounted interest rates for the most eligible buyers

- Some extra support tools such as education, calculators, online checklists, etc.

What Self-Employed Australians Should Know

Are you a freelancer, a small business-owner or self-employed? Low doc home loans are tailored for you. Just be informed about –

- Higher interest rates (because of perceived risk)

- More stringent lending rules (lower LVR, more scrutiny)

- Must show alternative income docs like BAS, invoices, accountant letters, etc.

The Role of Technology: How Are Digital Lenders Shaping the Game

Fintech lenders and digital banks are making it a lot easier than ever to compare different home loans. The core benefits include the followings –

- Fast approvals – some within 24–48 hours!

- Paperless applications through web or mobile

- More competitive interest rates courtesy lower overheads

- AI-driven recommendations and real-time rate comparison tools

With so many tech transformations happening, it’s now become easier to shop around. So, don’t settle for the first offer.

What to Watch for in 2025: Emerging Home Loan Trends

- Increasing Interest Rates: RBA cash rate movements will continue to affect loan affordability.

- Green Home Loans: Lucrative discounts for energy-efficient or sustainable properties.

- Greater Personalization: Loans designed for niche profiles (doctors, teachers or gig workers).

- Soaring Competition: More digital-only lenders and “neobank” disruptors.

Stay on top of these trends and revisit your loan within a few years to continue to save.

FAQs About Home Loans Australia

1.Fixed vs variable home loans? What’s the key difference?

Fixed home loan: The rate remains the same for a set period, safeguarding you from rate rises but providing less flexibility.

Variable home loan: The rate shifts with the changing market, often with additional features and the chance to benefit if rates fall.

There are many Australians that choose to split their loans for a combination of flexibility and certainty.

2. How much deposit do you need for a home loan in Australia?

Most of the lenders need at least a 5–20% deposit. A 20% deposit can help you avoid paying Lenders Mortgage Insurance (LMI).

3. Can I get a home loan with poor credit?

Yes, absolutely! Some lenders provide amazing options for borrowers with bad credit, but you can expect higher interest rates and a bit stricter condition.

Take Charge and Compare Home Loans Confidently

The suitable home loan can save you a fortune. Furthermore, it can help you conquer your financial and lifestyle milestones faster. Whether you’re buying your first home, investing, or refinancing, the potential is “now” in your hands—with better technology, greater options, and unprecedented access to lenders’ info.

Start to compare home loans as frequently as possible, understand each detail, and don’t be afraid of asking for a better deal. Your mortgage journey is only starting off, and it could be faster, smarter, and a lot less overwhelming.