Life presents numerous challenges that can significantly impact you. One such thing is navigating the world of private health insurance Australia! With changing policies, increasing premiums, and endless cover types available out there in the market, you may end up making a rushed decision.

Yet, choosing the right health insurance is more than just a financial choice. It’s rather more about securing your peace of mind, access to premium care, and even your long-term savings.

Let’s break it down—Australians have now become way more proactive than ever about their overall health coverage. In 2026, the best thing you can do is learn to compare health insurance, whether you're switching from a regular plan, upgrading to family coverage, or getting insurance for the first time.

To learn more, stay tuned!

A Quick Summary

Check out this blog to explore how you can confidently compare health insurance plans in Australia. Furthermore, brace yourself up to learn how to decode cover types, weigh premiums, decode the latest rules, and make a truly wise choice. Key takeaway? With these guidelines, you can easily compare private health insurance Australia to save you money, boost your benefits, and keep your peace of mind intact.

What Does It Really Mean to Compare Health Insurance Plans?

Comparing health insurance is not just about finding the most affordable premium. It’s about fulfilling your needs – family, health, and budget – with a plan that is suitable for you. In 2026, insurers provide a staggering range of products, and the “best” cover is generally different for everyone.

Why Should You Compare?

- Save on premiums:

Regularly assessing your policy can slash your costs.

- Upgrade your benefits:

New plans might come up with better hospital or extras cover.

- Avoid unexpected expenses:

Try to understand what’s covered before you need it!

- Fulfil new legal requirements:

Be updated with the latest private health insurance changes 2026.

So, are you all set to explore all the factors that truly matter? Let’s look at what you should compare, albeit beyond just the price tag.

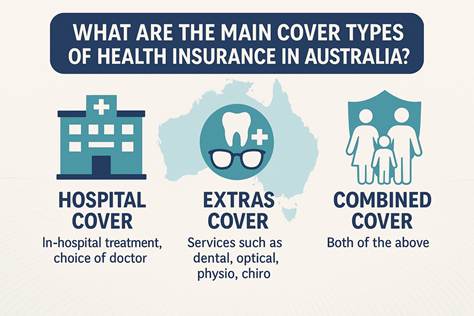

What Are the Main Cover Types of Health Insurance in Australia?

Not every policy is built the same! Here’s how some of the major cover types break down in Australia. Health insurance in Australia is divided into 2 main categories – Extras Cover and Hospital Cover.

Every plan is tailored to meet different needs and life stages, right from young couples to singles to growing families and retirees. Gaining an understanding of the difference between these cover types is paramount, especially if you want to compare health insurance options and pick the right balance between protection and cost.

- Hospital Cover vs. Extras Cover

| Type | What’s Covered | Who It’s For |

| Hospital Cover | In-hospital treatment as a private patient, choice of doctor | Anyone wanting more control over care |

| Extras Cover | Services such as dental, optical, physio, chiro, and more! | Those looking for optimum value on out-of-hospital extras |

| Combined Cover | Both of the above | Families and those wanting full protection |

Let’s explain things now in simple terms –

- Hospital cover usually safeguards you from big out-of-pocket costs in case you’re admitted to hospital.

- Extras cover helps with regular health costs not covered by Medicare.

When Should You Opt for Combined Cover?

No matter if you want peace of mind, you have kids, or expect regular dental/optical visits, a combined cover type could be the best option.

Core Features to Compare: It’s Not Only About the Premium

Always keep in mind, the premium isn’t the one and only factor you should consider, even though it’s crucial. A truly valuable policy goes beyond what you pay every month. The actual difference lies in when you get your money.

Think about factors like exclusions, inclusions, flexibility, and annual limits. By taking the time out to thoroughly assess every feature, you can easily avoid hidden costs and make sure that your cover matches your requisites – now and in the future.

1. Premiums and Payment Options

- You can compare how much you’ll pay annually or monthly.

- Always check for discounts in case you pay upfront or use direct debit.

- Factor in excesses as well as co-payments.

2. Inclusions and Exclusions

- What hospitals, treatments or specialists are covered?

- What gets excluded? (There are some policies that exclude certain therapies or surgeries.)

3. Benefit Limits and Waiting Periods

- Consider checking annual limits on extras (such as dental, physio, etc.).

- Review waiting periods for major treatments or pre-existing conditions.

4. Policy Flexibility and Portability

- Can you upgrade/downgrade without any hassle?

- Is there any portability perk especially if you switch funds?

Expert Take – “Australians often overtly emphasize premiums and completely forget to check annual limits or exclusions. The most effective policy is the one you can actually use at a price you can truly afford.” – Sarah L., Accredited Health Insurance Broker, Sydney

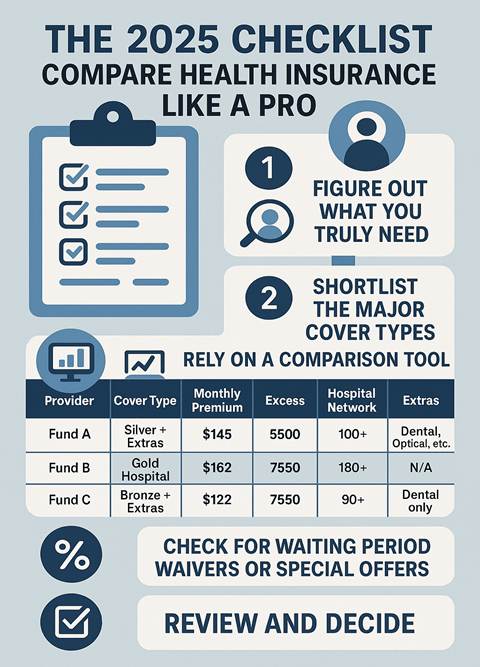

The 2026 Checklist: Compare Health Insurance Like A Pro

Let’s now walk you through a step-by-step process so that you never end up missing out a trick! By comparing health insurance is more effective when you break it down into actionable steps.

With an overload of offers and ongoing policy changes, having a clear-cut checklist makes sure that you cover every essential. Use this 2026 guideline as your roadmap to confidently review each plan and avoid common pitfalls, which catch many Australians off guard!

- Step 1: Figure Out What You Truly Need

- Age, family status, and any kind of health conditions

- Preferred hospitals or extras (such as dental, optical, physio, etc.)

- Step 2: Shortlist the Major Cover Types

- Hospital, Extras, or Combined?

- Gold, Silver, Bronze, or Basic tier?

- Step 3: Rely On a Comparison Tool

There are many reliable platforms available out there that allow you to compare health insurance policies side by side. Some of these platforms are Canstar, Privatehealth.gov, etc.

A Quick Comparison Table:

| Provider | Cover Type | Monthly Premium | Excess | Hospital Network | Extras |

| Fund A | Silver + Extras | $145 | $500 | 100+ | Dental, Optical, etc. |

| Fund B | Gold Hospital | $162 | $750 | 180+ | N/A |

| Fund C | Bronze + Extras | $122 | $750 | 90+ | Dental only |

Pro Tip – Make sure that you carefully read the PDS (Product Disclosure Statement) prior to making a choice.

- Step 4: Check for Waiting Period Waivers or Special Offers

- Some funds waive waiting periods for extras during promotions.

- Consider looking for discounts if you are signing up or switching as a family.

- Step 5: Review and Decide

- Double-check limits, exclusions, and the network of hospitals/providers.

- Make sure that your chosen policy perfectly fits your budget – now and if any circumstance changes.

Advanced Strategies for Comparing Health Insurance Plans

Now that you already know the basics of how you should compare health insurance in Australia, let’s now discover some easy yet effective strategies to access better care, save money, and stay abreast of the upcoming policy changes. This particular section will also cover FAQs, government incentives, and expert tips for 2026.

How Govt. Rebates and the Medicare Levy Surcharge Impact Your Premiums

Gaining an understanding of how government penalties and incentives affect your health insurance premiums can make a true difference to your out-of-pocket costs. The Australian Government provides valuable rebates to help decrease the cost of private health insurance Australia, while the Medicare Levy Surcharge acts as a financial nudge for higher earners to take out cover.

Understanding the way these factors actually work together will help you compare health insurance with more efficiency and make wiser financial decisions confidently!

- The Private Health Insurance Australia Rebate Explained

The Australian Government helps bring down the cost of private health insurance Australia through a means-tested rebate. Based on your age and income, you may qualify for a rebate of up to 32.812% on your premium (as of 2026).

| Age Group | Income Range | Maximum Rebate |

| <65 | Up to $93,000 (single) | 24.608% |

| 65–69 | Up to $93,000 (single) | 28.710% |

| 70+ | Up to $93,000 (single) | 32.812% |

Higher incomes receive lower or zero rebate. Couples or families always have higher thresholds.

- Medicare Levy Surcharge

In case you earn above a certain income or don’t haveprivate health insurance Australia hospital cover, you might have to pay the MLS (Medicare Levy Surcharge) of 1%–1.5%.

Pro Tip: Taking out eligible hospital cover can help you keep this surcharge at bay. Now you see why a suitable plan can save you on both taxes and premiums. Could you please share how one might effectively identify hidden costs?

Hidden Costs and Things You Should Watch Out For

While comparing, you should not only focus on the headline premium. Some health insurance plans may appear affordable initially, but they may entail hidden charges that could surprise you when you need to make a claim.

These might include exclusions for certain procedures, excess payments, or limits on how much you can claim for extras such as dental or physio. Being aware of all these details makes sure that you won’t be taken aback by unexpected out-of-pocket costs down the track.

Excess and Co-payments

- Excess: The upfront amount you pay while claiming hospital benefits.

- Co-payments: The amount you pay every day in hospital.

Gaps in Cover

- Not every treatment is included, even in higher-tier plans.

- Always check for exclusions and out-of-pocket “gap” payments.

Benefit Limits and Sub-Limits

- Extras cover often includes annual maximums per service (e.g., dental: $400/year).

- Some also have sub-limits (like major dental vs. general dental).

Pro Tips: How to Make the Most Value When You Compare Health Insurance

1. Don’t Ignore the Extras

- Extras can save you hundreds every year, especially if you use them.

- Consider optical, dental, and physio frequency in your household.

2. Compare More Than Just Price

- Hospital networks and direct-billing providers can make a huge difference.

- Some policies provide wellness extras such as gym discounts or telehealth.

3. Annual Review Is the Ultimate Key

- Insurers often change policies every April.

- Consider using reminders to compare health insurance every year before renewal.

4. Leverage Expert Support

- Accredited health insurance brokers can help in matching you to the right policy, often at no additional cost.

- There are many brokers that have access to special policy insights or offers, which aren’t widely advertised to the public.

- They can also assist with paperwork and claims, saving you a significant amount of time and reducing stress.

- Expert guidance makes sure that you avoid common errors and helps you in comparing health insurance policies depending on your actual requirements, not just marketing promises.

Chart: A Table for Comparing Health Insurance Plans

| Step | Action | What to Compare | Key Tip |

| 1 | List Your Needs | Hospital, extras, family size, etc. | What do you need most? |

| 2 | Shortlist Providers | Policy tier, networks, etc. | Gold/Silver/Bronze/Basic |

| 3 | Compare Costs | Premiums, rebates, excess, etc. | Look for waiting period waivers |

| 4 | Check Policy Details | Exclusions, limits, gaps, etc. | Read the PDS |

| 5 | Annual Review | New plans, price changes, etc. | Set a yearly reminder |

FAQs: Compare Health Insurance in Australia

1.What’s the best way to compare health insurance?

Make sure that you count on reliable government-backed tools such as privatehealth.gov.au for genuine and 100% unbiased comparisons. Go through the PDS carefully, and shortlist plans depending on cover types, not just cost.

2. When should you assess your health insurance plan?

- Every 12 months, or

- After life changes, such as marriage, having kids, health shifts, or turning 31 (to avoid Lifetime Health Cover loading)

3. How can you reduce your premiums?

- Opt for higher excess/co-payments in case you’re healthy.

- Make sure that you downgrade your cover type if your requirements have changed.

- Consider looking for private health insurance Australia funds with provider discounts or no-gap extras.

4. Is it really easy to switch health funds?

Yes, definitely! If you make a switch, waiting periods for the perks you’ve already served generally carry over, courtesy industry regulations.

5. What’s shifting in private health insurance in 2026?

There are some significant private health insurance changes 2026 that include new minimum standards for hospital tiers and clearer product labeling.

Make the Best Choice with Confidence

Selecting the right private health insurance Australia plan isn’t only about ticking a box but is also about freedom of choice, security, and the peace of mind that comes from knowing you’re covered when it matters most.

By snatching out the time to compare health insurance using these effective strategies, you’re not only saving money but also making a future-forward investment in your health and the well-being of your family.

Whether you want comprehensive cover types or just to reduce your premiums, the perfect solution is out there. So, are you ready to review your options? If yes, then begin your journey now – with confidence!