Ever looked at your health insurance renewal this year and wondered – “Why did my premium go up?” Or, maybe you’ve found yourself thinking, “What do the private health insurance changes 2026 actually include?”

With the government adjusting rebate thresholds, insurers revising tiers, and families facing a noticeable premium rise, Australians are now asking deeper questions about the real value of their cover.

Some households need practical clarity. Some need to understand whether their policy changes affect maternity, extras, or specialist services. Others simply want to know if a switch to another fund might save them money. That is exactly what this guide will help you understand.

A Quick Summary

The following are the biggest private health insurance changes 2026, including the updated policy changes, shifting rebate thresholds, and what's driving thepremium rise across insurers. You'll learn how these reforms impact households, what changed for extras and hospital cover, and how to adapt without overpaying. By the end, you'll know how to make smarter decisions using tools that help you to do an effective comparison of health insurance.

What's New in the Private Health Insurance Changes 2026

The reform package for private health insurance changes 2026brought in significant updates across the system. The changes are intended to increase transparency in the insurance market, ensure pricing fairness, and be long-term and sustainable.

Key changes include a new tiered system for policies and standardization of clinical definitions. This makes it easier for consumers to compare different insurance products.

The goal is to deliver better value and greater understanding for policyholders.

1. Changes to Rebate Thresholds

The Australian Government increased the rebate thresholds in line with growth in both incomes and healthcare inflation.

What Changed?

- The income bands were adjusted upwards.

- More households now qualify for a partial rebate.

- The base tier drops slightly to 24.288% (under 65) from April 1, 2026

2. Annual Premium Rise Across Most Insurers

Industry-weighted average: 3.73% effective April 1, 2026 (e.g., Bupa at 5.10%, Navy Health at 2.85%). Variations by fund, but extras and hospital rose similarly.

3. Mandatory Policy Changes Introduced in 2026

In that light, several policy changes came into effect to ensure greater transparency and clearer categorization for consumers.

What Changed?

- Updated Gold/Silver/Bronze/Basic tier rules

- Revised definitions of high-cost services (e.g., orthopedic, cardiac)

A Quick Comparison Table: What Actually Changed?

| Category | 2024 | 2026 | What It Means for You |

| Rebate Thresholds | Singles: ≤$97,000 Families: ≤$194,000 | Singles: ≤$101,000 Families: ≤$202,000 (from July 1) | More households qualify for partial/full rebates (Tier 1 up to $118k/$236k) |

| Average Premium Increase | ~3.1% | 3.73% (from April 1) | About $80–$150 more per year; rebates offset approximately. 24–32% |

| Mental Health Benefits | Optional upgrades | Optional (PHI extras for counselling; Medicare MBS updates Nov 1) | Easier access through Medicare–extras integration; no PHI mandate |

| Hospital Tier Rules | Existing definitions | Updated clinical categories | Clearer, more consistent hospital coverage across all funds |

| High-Cost Services | Varied by fund | Standardized definitions | More transparency on out-of-pocket costs for orthopedic/cardiac care |

Disclaimer (as of Nov 15, 2026): All PHI data here is from official ATO/Health Dept sources. Verify your policy at privatehealth.gov.au for the latest, as changes like rebates index annually.

Expert Quote: “We’veworked hard to make sure Australians get a fairer, better-value deal from private health insurers in 2026. These changes are about keeping premiums as affordable as possible while still supporting quality care.”— Hon Mark Butler MP, Minister for Health and Aged Care

Why These Private Health Insurance Changes 2026 Matter for Australians

- Larger Gaps Between Policy Tiers

The revamped categorization made the difference between bronze, silver, and gold policies much clearer and more expensive. Some families were "pushed upward" when certain benefits moved to higher tiers.

- Out-of-Pocket Costs Continue to Climb

Even with rebates, health care inflation drove higher personal spending.

Key Cost Drivers

- Hospital costs have climbed by 9.4%, specialist fees are up around 7% with average gaps rising to $210, and allied health services like dental and physio have seen a general increase of about 3.2% heading into August 2026.

This is one reason why many households these days consider comparing extras cover to prevent unnecessary spending.

- More Flexibility in Extras Policies

Among the positive policy changes in 2026 was the introduction of flexible extras bundles.

What Improved

- Pick-and-mix extras

- Adjustable annual limits

- Higher rollover allowances

- No-gap dental enhancements in selected funds

This flexibility is especially beneficial to families who use dental, physio, or optical benefits often.

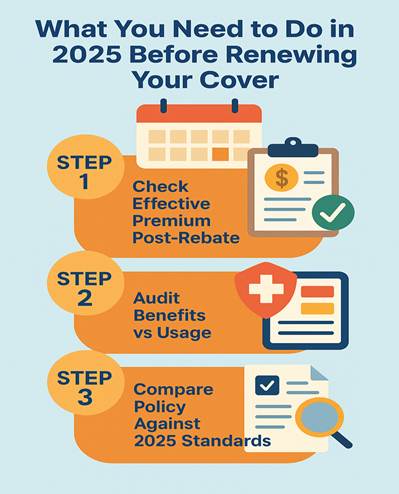

What You Need to Do in 2026 Before Renewing Your Cover

Most of the Australians are now reviewing their policies far more closely in 2026. Here’s how to approach it with efficiency and more confidence.

- Step 1: Check Your Effective Premium Post-Rebate

Don't rely on the advertised amount. Calculate what you'll pay after the revised rebate thresholds.

- Step 2: Audit Your Benefits vs Usage

If your usage is low, you may downgrade. If your kids need braces or you're planning for pregnancy, upgrade your family health cover Australiawith caution.

- Step 3: Compare Your Policy Against New 2026 Standards

This new framework changed several inclusions. That is why it is considered the ideal time to compare health insurance.

FAQs on Private Health Insurance Changes 2026

- Why did premiums rise so much in 2026?

This was because of healthcare inflation, rising hospital costs, and increased claims. It has finally made the insurers increase the premiums significantly.

- Did all policies change under the 2026 regulations?

Most did. Tier adjustments and service reclassification affected nearly all funds.

- Are rebates higher in 2026?

Yes, absolutely – mainly because of the updated rebate thresholds. More Australians qualify for partial rebates.

- Should I upgrade my cover?

Only if your key services are moved into a higher tier under the new policy changes should you consider upgrading your cover.

The Closing Note

Private health insurance changes 2026 ushered in significant pricing, benefit, rebate, and policy structure changes. For many Australians, the value of cover will now be determined by smart decisions, rather than default renewals. Review your inclusions. Re-evaluate your tier. Check your actual premium after rebates.

And whenever possible, do clear extras cover comparison to avoid unnecessary costs. With a proper strategy in place, you can safeguard your health and wallet, even in the year of rapid change. Savvy shoppers will find that now is the perfect time to optimize their coverage and savings.