Are you planning to buy the house of your dreams soon? Great! But stuck in a dilemma between fixed vs. variable home loan?Are you wondering which type of loan is suitable for you? In this case, you should opt for a fixed loan. If you prefer loan flexibilityjust because you want to save when the rates drop, you should zero in on a variable loan.

If you are still cloudy about what these loans truly mean or the benefits they bring to the table, then read on in this guideline. This blog will provide you with a comprehensive understanding of both these options. Armed with the right knowledge, you can easily make a confident, money-smart decision for your future.

A Quick Summary

The big debate around fixed vs. variable home loanis on! Wondering which one is right for you? This blog explains in simple terms their differences, perks, and potential drawbacks. Brace yourself to learn how factors like interest rate predictability, loan flexibility, and your daily needs can affect your choice.

Key Takeaway: The fixed loans come up with stability, while variable loans always offer flexibility. Your most suitable fit depends on your financial plans, risk appetite, and the current market trends.

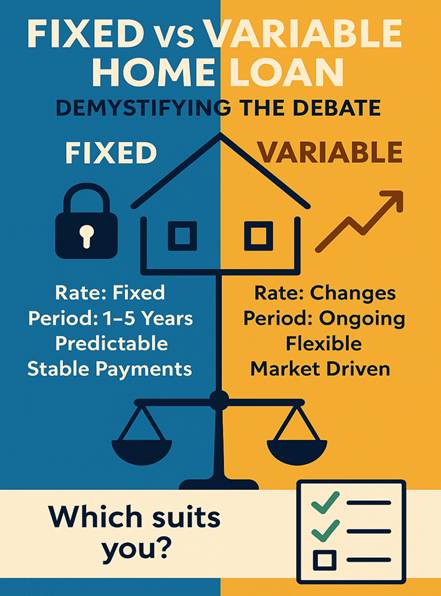

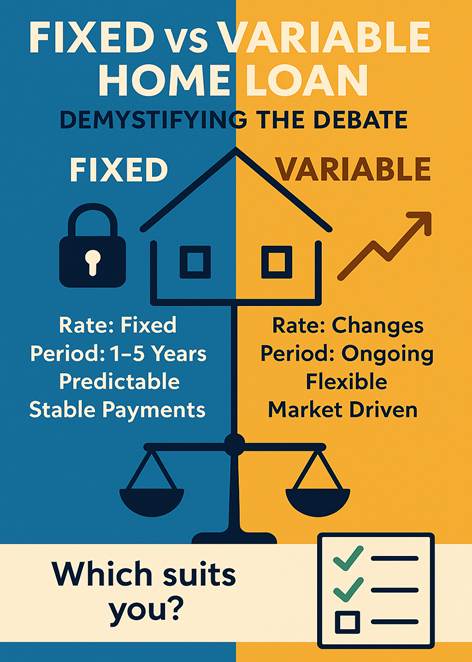

Fixed vs. Variable Home Loan – Demystifying the Debate

Before you go further into the discussion around fixed and variable loans, let’s first understand their basics.

- Understanding the Basics

Let’s begin with a crystal-clear definition of both of them –

- Fixed Home Loan:

Your interest rate stays the same for a set period (typically 1–5 years).

- Variable Home Loan:

But, in this case, your overall interest rate can soar or drop with the changing market.

Fixed vs. Variable Home Loan: A Quick Table on Their Key Features

| Feature | Fixed Home Loan | Variable Home Loan |

| Interest Rate | Locked in | Changes with the evolving market |

| Repayments | Predictable | Might soar or fall |

| Loan Flexibility | Limited | High |

| Offset/Redraw | Sometimes limited | Usually allowed |

| Break Fees | Could be slightly high | Typically, none |

| Best For | Stability seekers | Flexible borrowers |

Expert Take: “Making a pick between fixed and variable loans isn’t just about rates. It’s rather about matching the loan you take up to your daily lifestyle and risk comfort. Ask yourself: do you need stability? Or, are you okay with betting on rate drops for potential savings in the future?” – Sarah Megginson, Money.com.au property editor

- How Does Interest Rate Predictability Vary?

- Fixed Rate:

Interest rate predictability is the ultimate name of the game! You know your repayments for the set period, perfect for budgeting and keeping your peace of mind intact.

- Variable Rate:

Your repayments differ. When rates drop, you can save significantly. If rates go up, so do your costs. There is less predictability but potentially more rewards.

Quick Stat: As of the year 2024, approximately 70% of Australian home loans are variable, but fixed loans increased during COVID-era rate cuts (APRA, 2024).

Advantages and Disadvantages: Fixed vs. Variable Home Loan

Here are some advantages and disadvantages of both fixed and variable home loans.

- Fixed Home Loans: Pros and Cons

Pros

- Interest Rate Predictability

Know exactly what you will pay every month.

- Budget Control

Ideal for first-time home buyers and families that demand certainty.

- Protection From Rate Hikes

You are safe in case the Reserve Bank maximizes the rates.

Cons

- Loan Flexibility

Often less flexibility puts limitations on additional repayments, redraws, or offset accounts.

- Break Costs

Planning to leave early? Expect hefty exit or “break” fees.

- No Benefit If Rates Fall

You are locked in, even if the variable rates go down.

- Variable Home Loans: Pros and Cons

Pros

- Loan Flexibility

Easily make additional repayments, access redraws, or make use of offset accounts.

- Benefit from Rate Cuts

If interest rates drop, so do your repayments!

- Easier to Switch

Usually no break costs, which makes it easier to refinance.

Cons

- Interest Rate Predictability

Repayments can shoot up, making budgeting a bit more challenging.

- Potential for Higher Costs

If rates climb, your costs jump too.

- Less Certainty

This type of loan is not suitable for individuals who prioritize stable and predictable outgoings.

Next, let’s see which situations complement each type of loan.

Fixed vs Variable Home Loan – Who Should Pick What?

- When Fixed Rates Win

- You want certainty, perfect for families or those on a stringent budget.

- You expect rates to shoot up soon.

- You’re risk-averse and such as planning ahead.

- When Variable Rates Matter

- You can deal with potential rate hikes.

- You demand the freedom to pay off your loan faster.

- You prefer flexibility. Maybe you will move, refinance, or switch loans.

Split Loans: Explore The Best of Both Worlds!

You can actually split your loan. Part fixed, part variable – some amount of security, some bit of flexibility.

Fixed and Variable Home Loans: Real-World Scenarios

- Scenario 1: First-Home Buyer in Sydney

- Fixed: This locks in your repayment, useful if you’re stretching your budget for your first house.

- Variable: May suit in case you’re confident that the rates will drop or want the option to pay an additional amount when you can.

- Scenario 2: Growing Family Upgrades in Melbourne

- Fixed: It eliminates repayment surprises, which is perfect with big family expenses.

- Variable: Works well if you expect to sell or refinance anytime soon.

- Scenario 3: Investor in Brisbane

- Fixed: Predictable expenses for your rental property.

- Variable: Benefit from rate drops, and use offset/redraw to address cash flow.

A Quick Table: Fixed vs. Variable Home Loan Outcomes

| Borrower Type | Fixed Loan (Best If) | Variable Loan (Best If) |

| First Home Buyer | Need budgeting certainty | Expect to pay off faster |

| Family Upgrader | Want payment stability? | Plan to refinance or move |

| Investor | Value predictable expenses | Want to leverage offset/redraw |

Let’s Clear Up the Last Bits – FAQ Time!

1. Can you easily switch from fixed to variable later?

Yes, absolutely! But, in that case, you may have to break costs on the fixed loans. Make sure that you thoroughly check with your lender prior to making any decision.

2. How long can you fix your rate?

Most of the lenders in Australia provide both fixed rates for 1–5 years. Some might go up to 10 years, but it’s rare!

3. What about split loans?

A split loan combines both variable and fixed loans. Thus, it enables you to enjoy both of the perks – stability and flexibility.

4. Do fixed loans have redrawn or offset features?

Often, but not always. There are many variable loans out there that provide more loan flexibility for redraws and offsets.

5. How do you find the best option?

Make sure that you carefully compare home loans from multiple banks. Furthermore, take your risk appetite and plans into serious consideration.

6. Where can you learn more?

To glean accurate insights, check out these reliable resources –

- Moneysmart: Learn about the different types of home loans that are explained.

- Canstar: Explore details related to Fixed vs variable interest rates

- Finder: Check this platform to decide if you should fix your rate or not!

Here’s the Final Verdict

There’s no “perfect” answer to the debate around the fixed vs. variable home loan. Your perfect loan depends on your daily lifestyle, risk tolerance, and future plans. If you want interest rate predictability and stable repayments, a fixed loan is the way to go! In case you prefer loan flexibility and the promising potential of a giant saving when rates drop, a variable loan should be your ideal pick!

The Key Takeaway

Fixed vs variable home loan? Compare smartly, align things with your goals, and explore different split options or low doc home loans for further flexibility.